How Indexed Universal LIfe WOrks

Discover how wealthy people have leveraged cash value life insurance policies for over 200 years to grow their money and avoid paying taxes legally!

Discover How We Help Individuals and Small Business Owners protect their financial future using The Little-Known Index Universal Life Insurance Policy That Industry Giants Can't Seem To Stop Talking About...

Unlock compounding interest, enjoy tax-free retirement income, and protect yourself with living benefits & leave a legacy for your loved ones.

Frequently Asked Questions

Indexed universal life insurance is a type of permanent life insurance that has a cash value component in addition to a death benefit. The money in your cash value account can earn interest based on a stock market index chosen by the insurance company, such as the S&P 500.

When a premium is paid, a portion of the premium pays for the cost of insurance, and the difference goes into the cash value account. Based on how the stock market index performs, the cash value can be credited 5-10% interest annually. Note: your money is not invested directly in the market, so you never lose what you have accumulate in your cash value when the market goes down.

Below is our recommendation:

20yrs - 25 yrs: $150 - $200

26yrs - 30 yrs: $200 - $250

31yrs - 35 yrs: $250 - $300

36yrs - 40 yrs: $300 - $350

41yrs - 45 yrs: $400 - $450

46yrs - 50 yrs: $500 - $550

50yrs- 60yrs: $550 - $1000 or more

There are many advantages to having an IUL policy:

Less risk: The cash value is not directly invested in the stock market, thus reducing risk to zero.

Interest rate ranges from 5 -10% annually (Depending on the indexed performance)

Tax free- You don’t pay taxes on interest earned

Easy distribution: The cash value in IUL policies can be accessed at any time without penalty, regardless of a person’s age.

Retirement Supplement: When structured and funded properly it can be used as a tax free retirement income

Access death benefit: Yo can access 80-100% of the death benefit if you become Critically, Terminally, or Chronically ill.

Death benefit: This benefit is permanent, not subject to income or death taxes, and not required to go through probate.

Unlimited contribution: IUL insurance policies have no limitations on annual contributions. This means you can put in extra money in the cash value and earn interest on it.

Anyone from 15 days old and above can qualify for an IUL

Generally, IUL policies does not require medical exams. However, during the application process, you will need to give HIPPA consent to the insurance company to access your medical record to make sure that you do not have any major health issues. In some cases, medical exam may be required based on medical history.

Also, if you applying for a death benefit of more than $1 million, a medical exam might be required.

Below are some of the reasons why a person can get denied for IUL:

-A felony within 5-10 years

-DWI or DUI within 5 years

-Overweight (Depends on height)

-Personal history of cancer

-History of alcohol or substance abuse

-Life, health, or disability insurance that has been rated or declined

-Major medical conditions

-Alcohol Abuse

No, you do not pay taxes on funds accessed from the policy as a loan and the policy remains enforces. If you decide to cancel the policy you will be required to pay taxes on any "interested earned'' in your cash value.

Yes, you are allowed to increase your premium up to a certain amount annually depending on how your policy is strcutured.

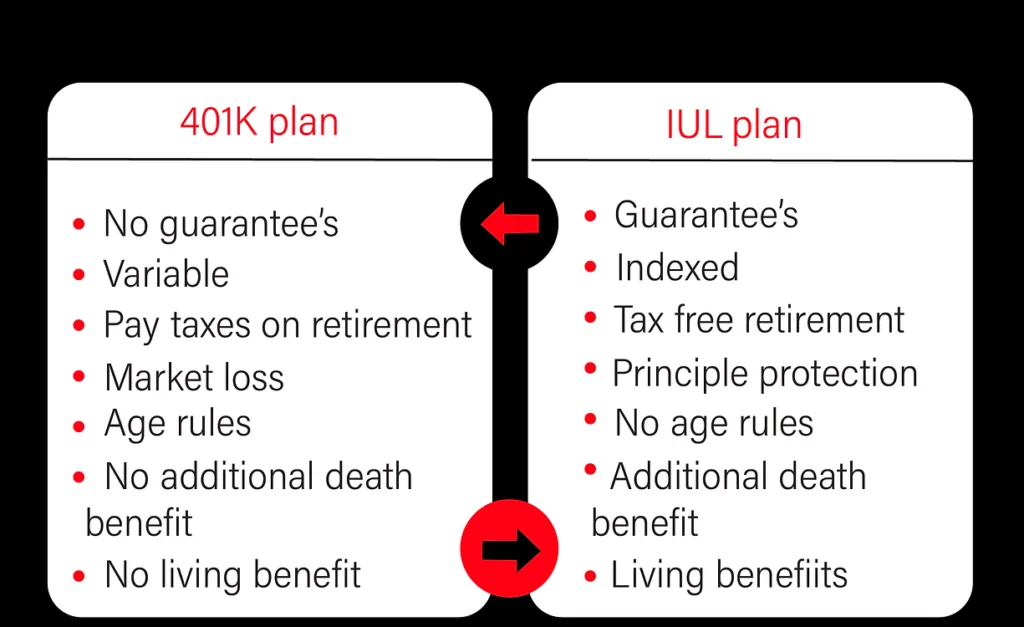

401k and IRA are both considered investments, while IUL is not. However, IUL does offer several benefits, which are not available with both 401k and IRA. (i.e. protection from market volatility.

For example, you can fund the policy with as much as you want, there are no age restrictions on withdrawals, you do not have to pay taxes on the interest earned, it's not impacted by market losses etc.

IUL's cash value growth is based on the stock market indexed performance, as a result there is a higher probability of receiving a higher interest rate up to 10% or more. On the other hand, Whole Life cash value growth is based on the company's performance, so the maximum interest rate is often capped around 5%.

Generally, it takes 5- 10 years for you to accumulate enough funds to withdrawal, and the minimum you can withdrawal is $500. However, you can access funds in your cash value after 12 months "IF" you put in a lump sum.

The cash value is added to the death benefit and paid out to your beneficiary. For example, if you pass away and you have $50,000 in cash value and $300,000 in death benefit, your beneficiary will receive a total of $350,000.

Yes, but it depends on how much your death benefit it. A high death benefit gives you the ability to over fund the policy with more money, which then enables your cash value to grow much faster.

You can either withdrawal the cash value, which will reduce or deplete what you have accumulated, or you can take out a loan against the cash value.

It is more beneficial to take out a loan. When the insurance company gives a loan they are not necessarily taking it from your money. Your money is being held as a collateral against the loan, which means you earning uninterrupted compound interest.

If you do pass way in the process of paying back your loan, the loan balance will be deducted from your cash value and whatever is left will be paid out to your beneficiary.

When an insurance company becomes financially unstable and can’t pay policyholder claims, the state’s insurance commissioner can take over the company through a process called receivership. First, the commissioner will try to rehabilitate the company to improve its financial situation. If that doesn’t work, the commissioner can declare the company insolvent and sell off its assets, according to the National Organization of Life & Health Insurance Guaranty Associations.

If an insurance company is declared insolvent, the state guaranty association and guaranty fund swing into action. The association will transfer the insurer’s policies to another insurance company or continue providing coverage itself for policyholders.

You can only get an IUL through a licensed insurance agent who is appointed with specific carriers that offers IUL. Our agents are licensed nationwide with several carriers that offers IUL.